2019 Q3 Review - Consolidation ends with sudden drop

Having recently dipped below the 200-day moving average, the total crypto market cap has again entered a bear market. The total cryptocurrency market cap ended Q3 down ~26%, giving back a quarter of Q2’s mammoth gain. In general, trading volumes across all assets have decreased substantially from Q2.

Additionally, an upcoming 50-day and 200-day moving average cross will end the 150-day bullish trend established at the beginning of Q2.

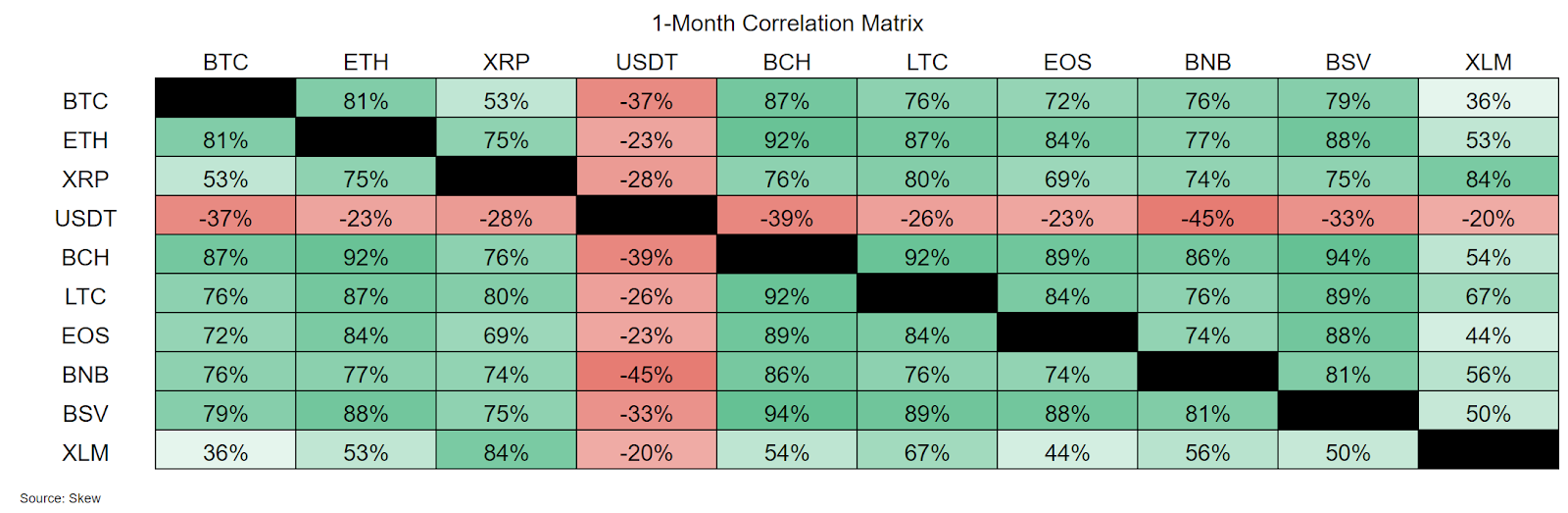

The majority of high market cap coins have been highly correlated over the past month. Tether (USDT) has had the strongest inverse correlation will all assets, while Binance Coin (BNB) has had the strongest inverse correlation to USDT, at -45%.

BTC has seen a strong positive correlations across the board, with all non-stablecoin assets, but has seen a weak positive correlation with Ripple (XRP) and Stellar (XLM). Bitcoin Satoshi’s Vision (BCHSV) and Bitcoin Cash (BCH), both Bitcoin forks, show the strongest positive correlation at 94%.

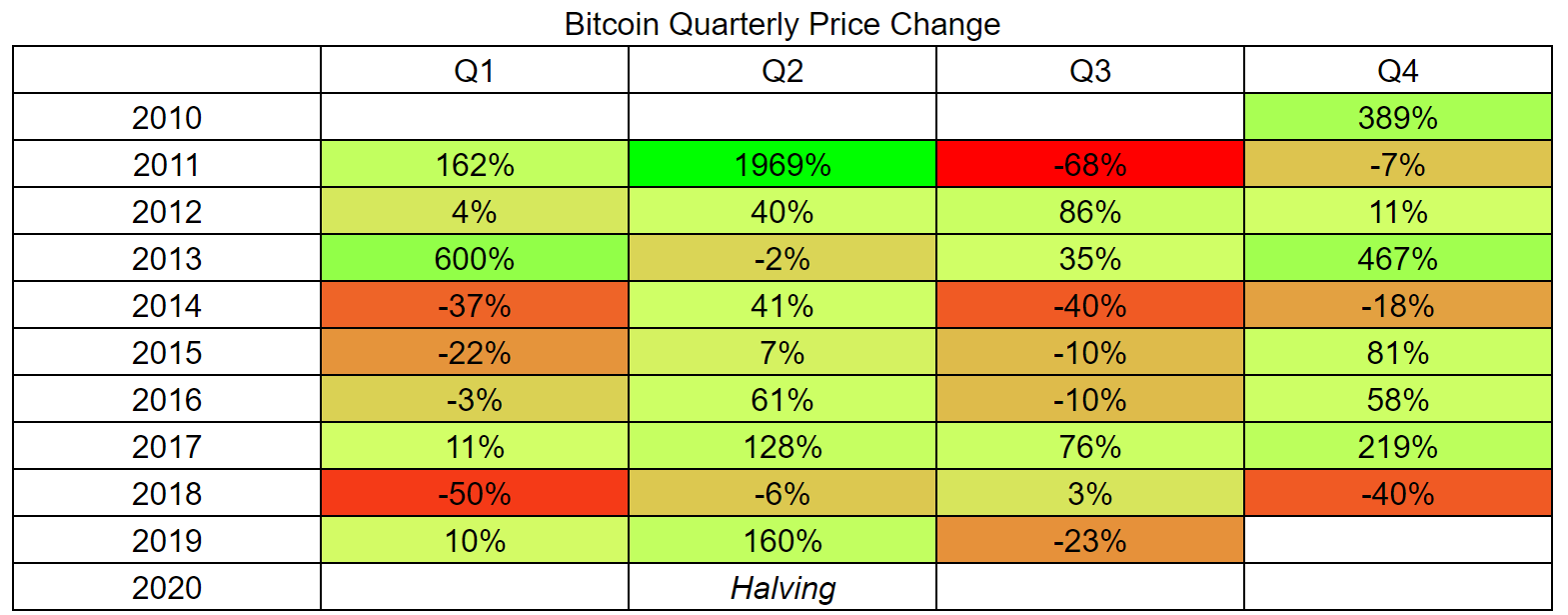

Q3 Price Changes Match Historical Norms

Historically, relative changes in BTC price have been closely related to three-month cycles. These quarterly cycles often see a dramatic expansion or contraction in price, with very few quarters ending with less than a 10% price change. Q2 and Q4 of any given year have been the most positive periods, while Q1 and Q3 have been the most negative periods.

In total, there have been 21 positive quarters and 14 negative quarters. Bitcoin’s massive Q2 2019, at +160%, is the seventh-best quarterly gain. The highest positive period was Q2 2011 at +1941%, and the highest negative period was Q3 of the same year at -68%. Q3 2019 marked the fifth negative Q3, which now has the most negative periods of any other quarter.

The average gain among all positive periods, excluding Q2 2011, is 126%, while the average loss among all negative periods is -24%. The longest period of consecutive gains occurred between Q4 2016 and Q1 2018, totaling 484%. The longest period of consecutive losses occurred between Q3 2014 and Q2 2015, totaling 80%.

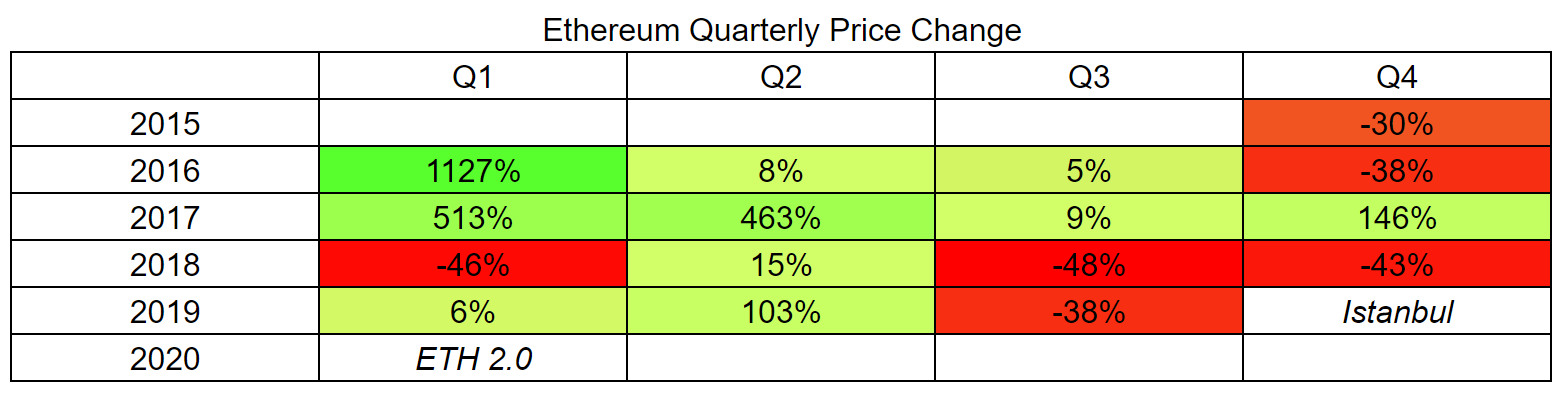

ETH has had 16 total trading quarters, far fewer BTC, but most of ETH’s price changes within each quarter have been very similar. Negative quarters have historically had a tight range of -30% to -48% whereas positive quarters fit into three ranges: <+20%, around +100%, or >+500%. The average gain among all positive quarters, excluding Q1 2016, is +141%, and the average loss among all negative quarters is -40%. ETH has only outperformed BTC in 6 quarters.

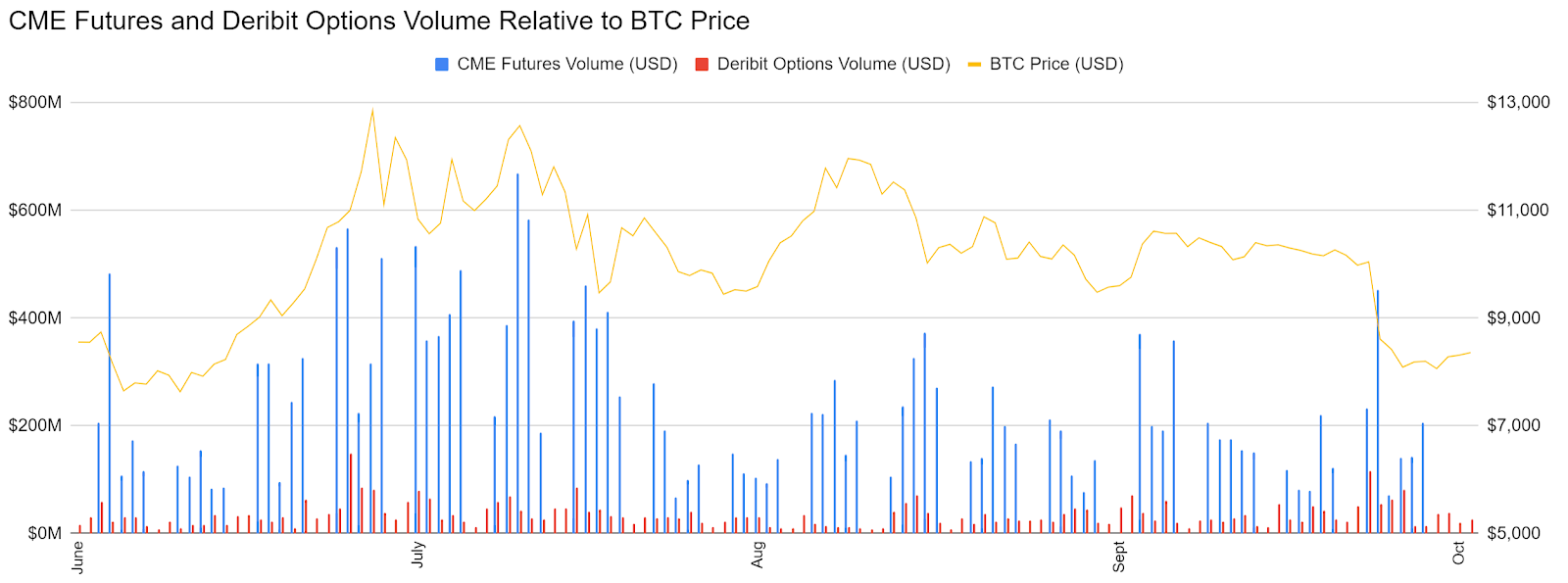

Furthermore, the opening and expiration dates of futures and options markets have had an increasing influence on price. Volume and price volatility has typically increased near each contract rollover period.

The Chicago Mercantile Exchange (CME), which facilitates the largest portion of derivatives contracts in the world, launched a cash-settled BTC futures contract in December 2017. Deribit BTC options launched in September 2018 and have become increasingly popular. CME announced a BTC options product coming in Q1 2020.

On-chain Activity Cools Down as ASICs Heat Up

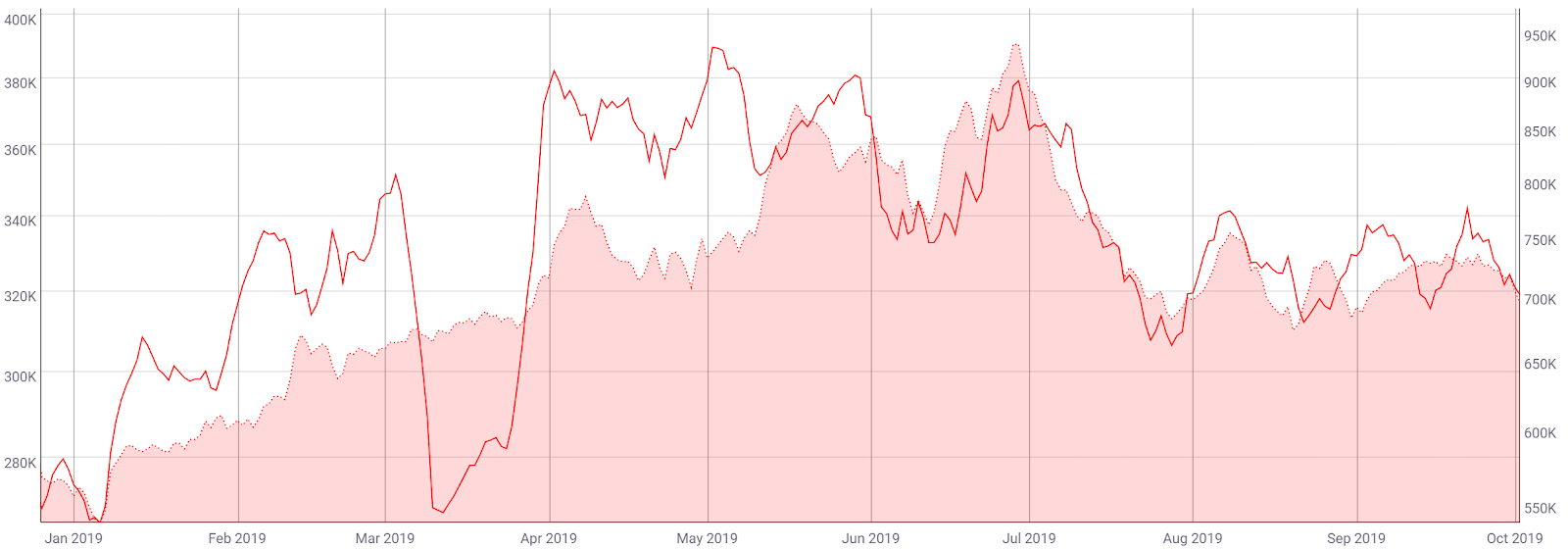

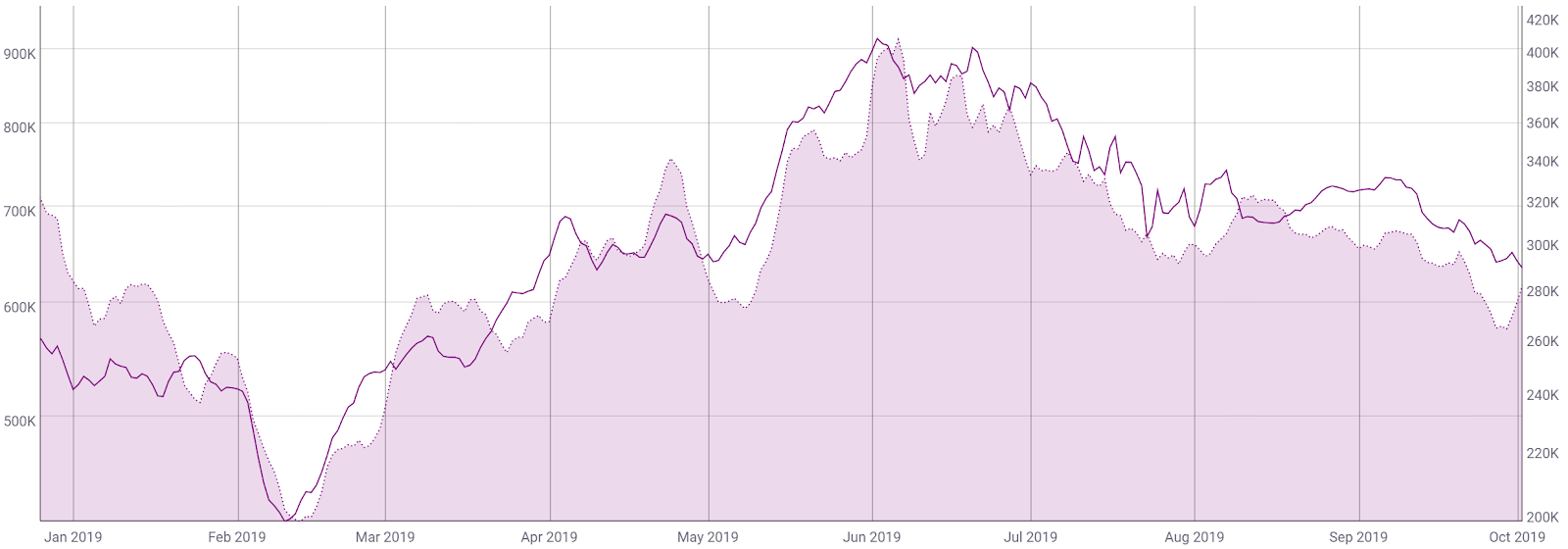

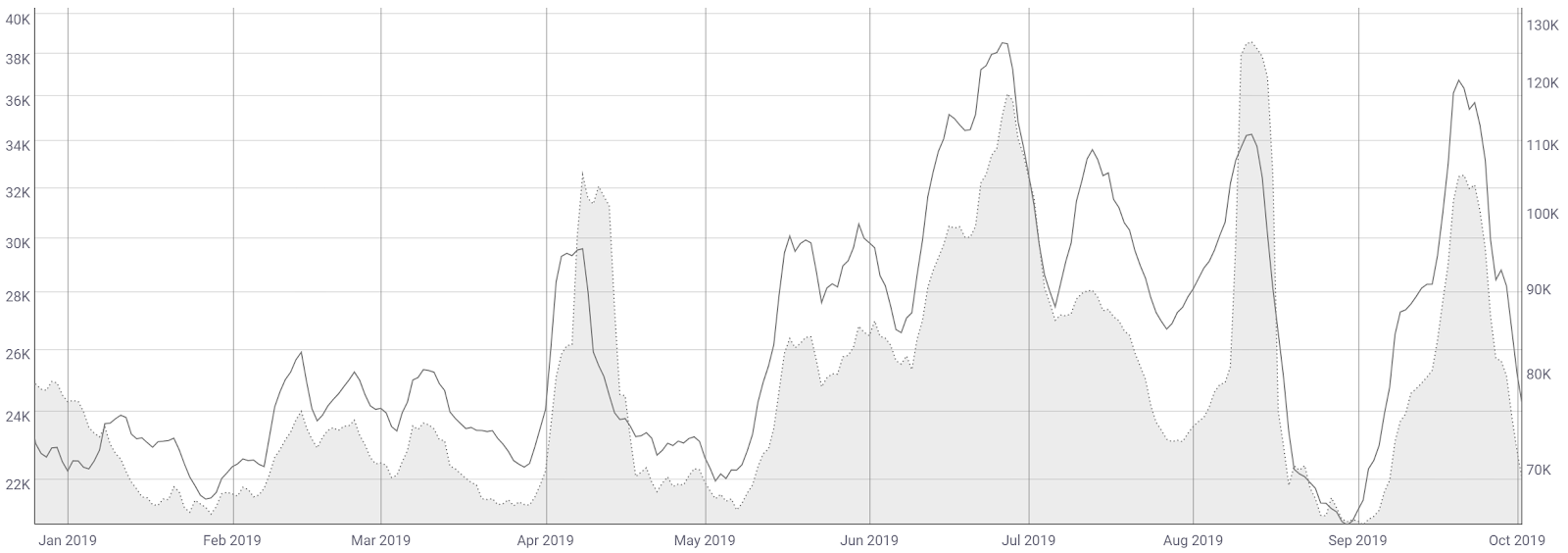

Metrics tracking on-chain activity for the top coins and assets decreased or remained stagnant throughout the quarter. Both average transactions per week (line, charts below) and weekly active addresses (fill, charts below) saw sustained increases for BTC, ETH, XRP, BCH, and LTC. The spike in BCH transactions and active addresses was related to a stress-test on the chain. LTC experienced a block reward halving this quarter, which likely played a role in the rollercoaster of on-chain activity.

Bitcoin (BTC) average transactions per week & weekly active addresses. Source: CoinMetrics

Ethereum (ETH) average transactions per week & weekly active addresses. Source: CoinMetrics

Ripple (XRP) average transactions per week & weekly active addresses. Source: CoinMetrics

Bitcoin Cash (BCH) average transactions per week & weekly active addresses. Source: CoinMetrics

Litecoin (LTC) average transactions per week & weekly active addresses. Source: CoinMetrics

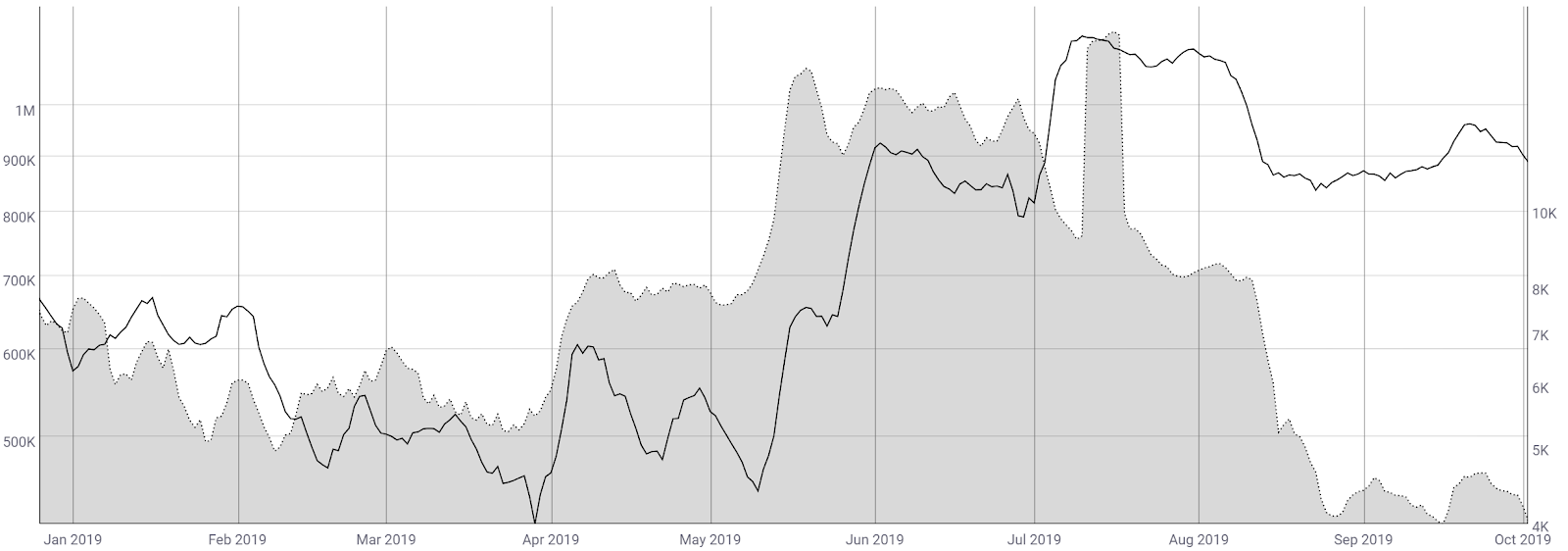

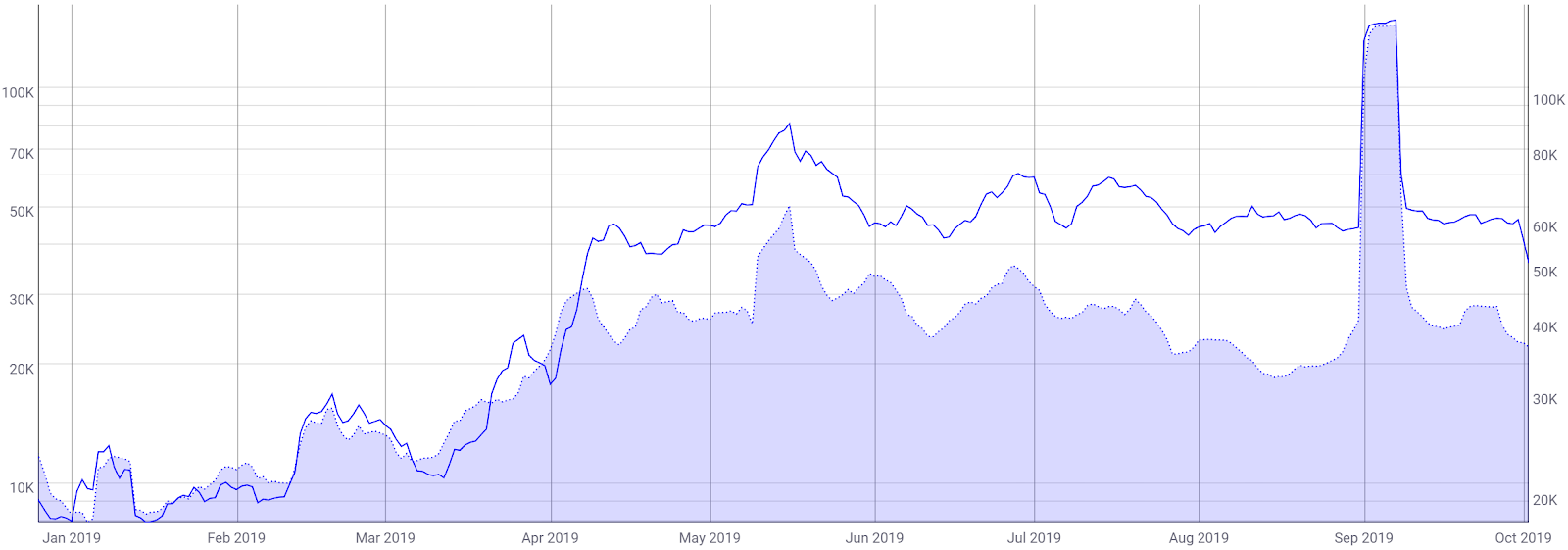

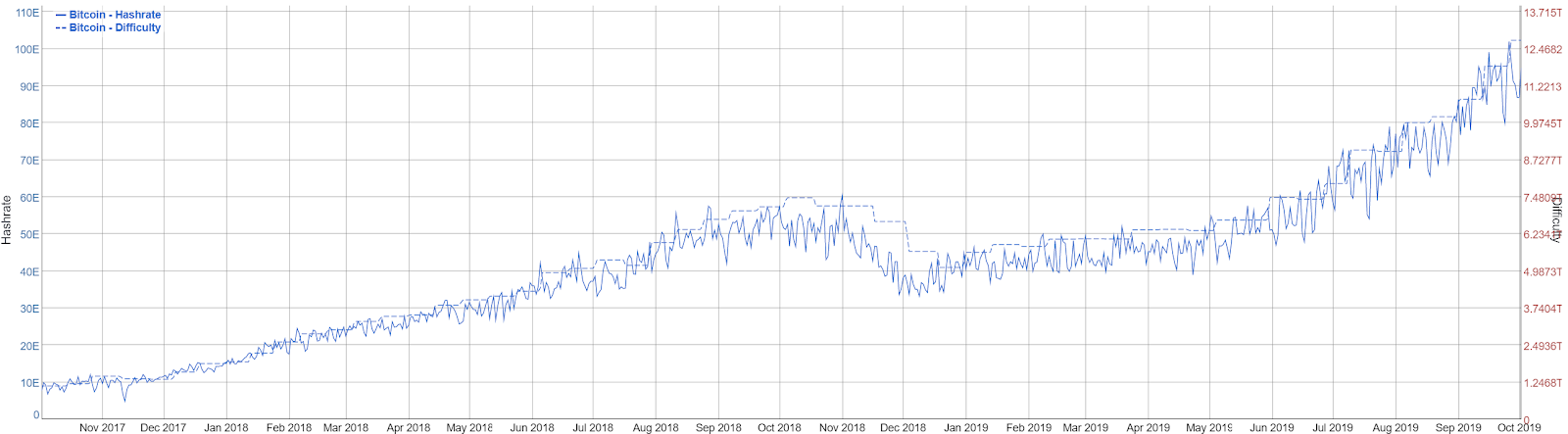

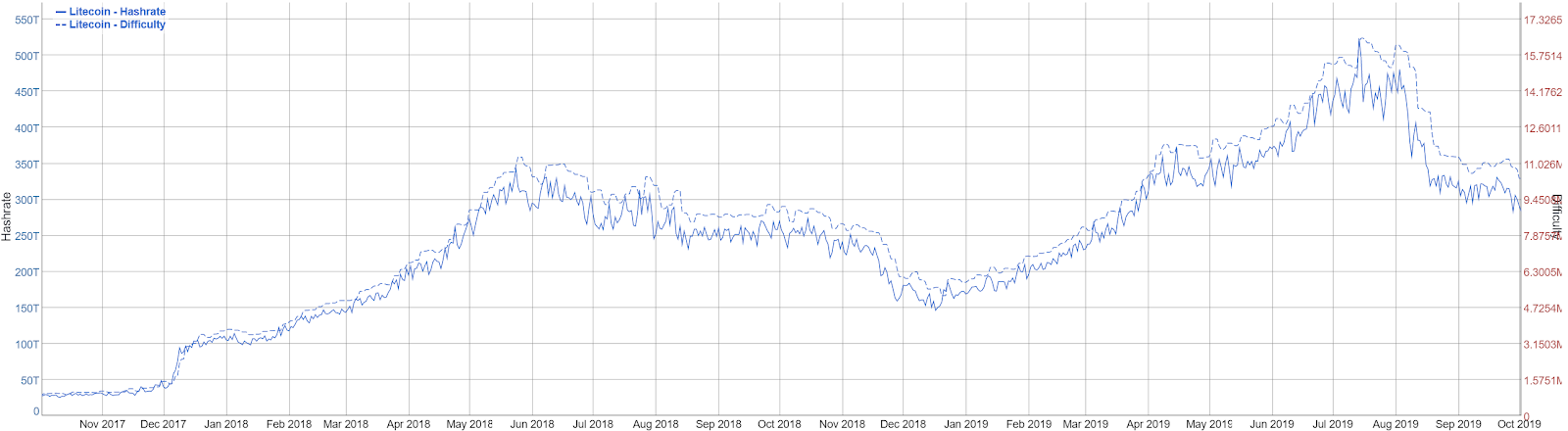

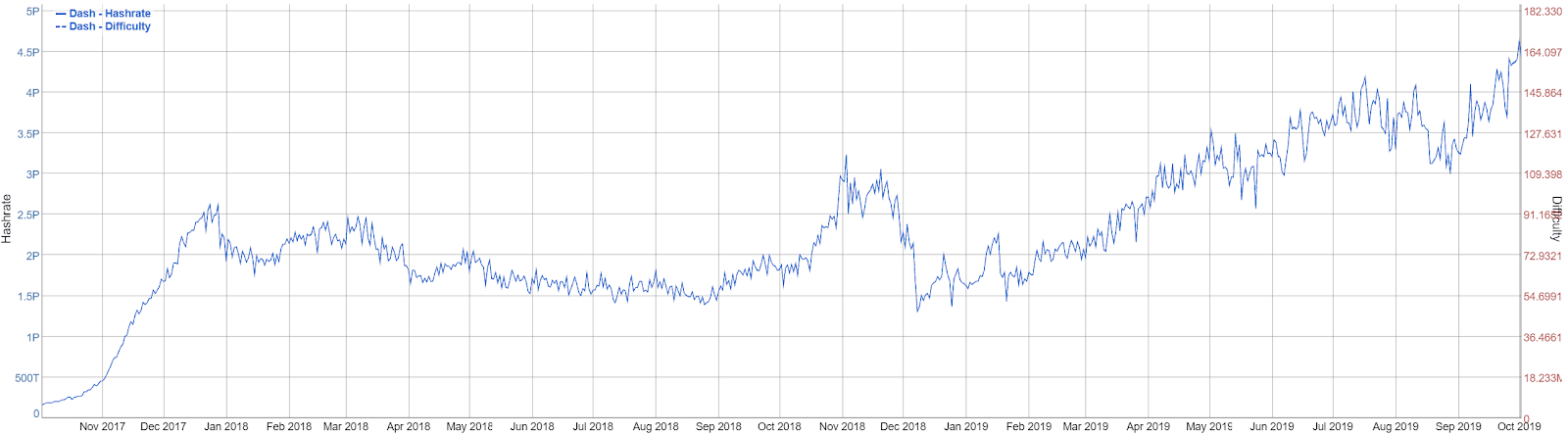

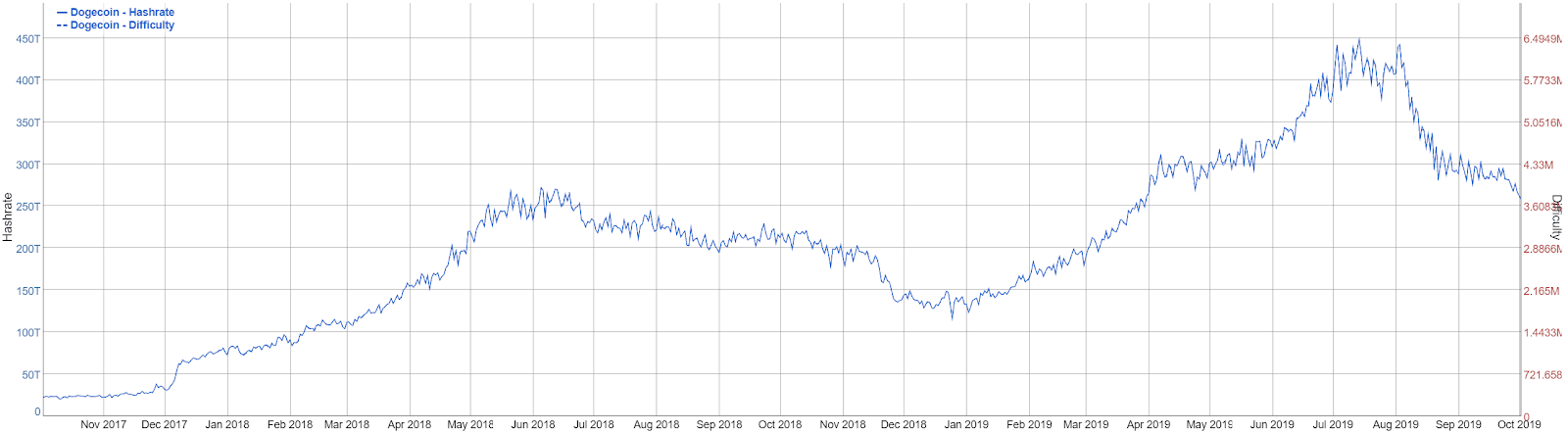

Mining metrics show that hash rates and difficulty for many coins using Proof-of-Work (PoW) algorithms continued to explode. This can be attributed to; cheap electricity globally from renewable energy sources, an increase in ASICs manufactured, and heightened efficiency of those new ASICs. Hash rates and difficulty hit record highs for BTC, LTC, DASH, ZEC, and DOGE this quarter.

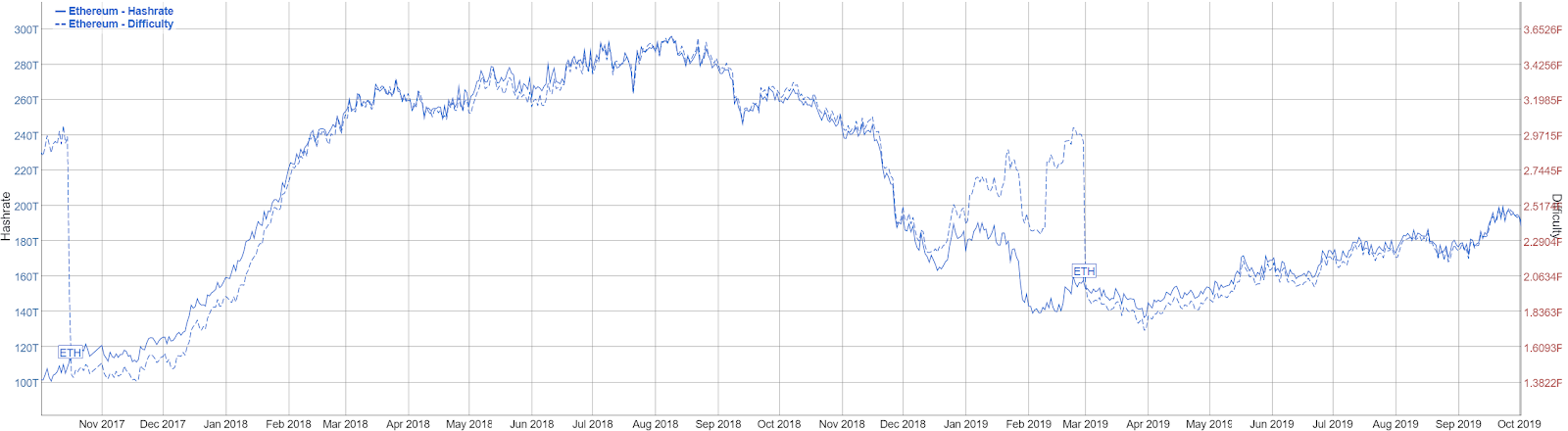

Again, the LTC halving played a role in both the LTC and DOGE hash rates. DOGE is merge-mined with LTC. The ETH hash rate is well-below the record high, but has increased steadily since April, after the most recent difficulty bomb and block reward adjustment. ETH is set for a change to it’s PoW algorithm, to ProgPoW, sometime in the next six months, in an effort to decrease ASICs used on the chain.

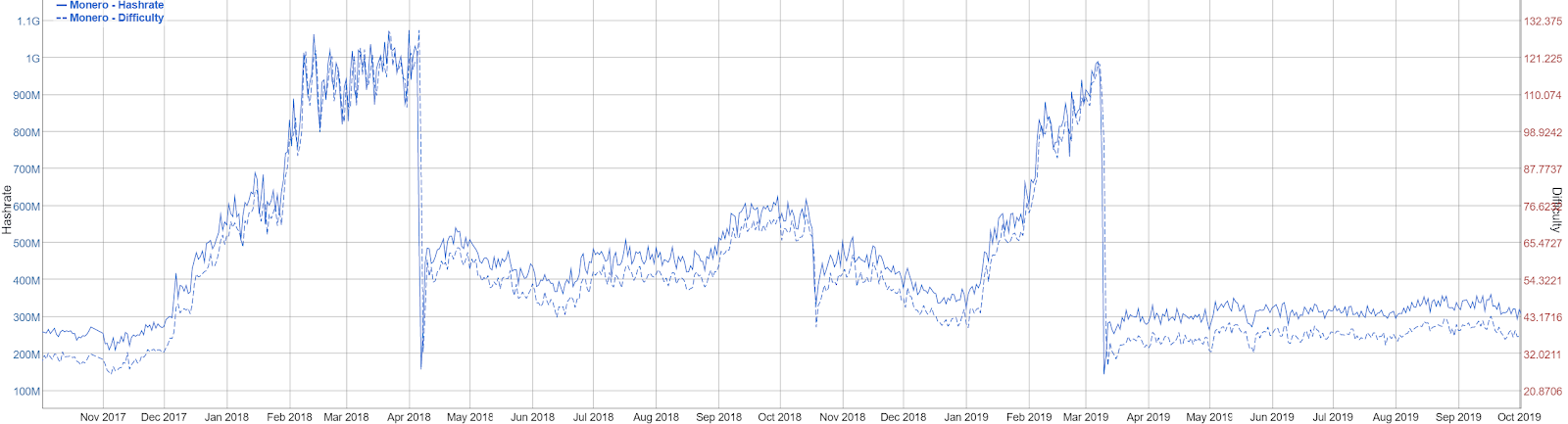

XMR, which is developed with a staunch anti-ASIC approach through recurring algorithm adjustments, had no large deviation in hash rate or difficulty throughout the quarter. Additionally, XMR is scheduled to change it’s PoW algorithm to RandomX, which is optimized for CPU mining. This will drop the efficiency of both GPUs and ASICs mining on the chain dramatically.

Bitcoin (BTC) hash rate & difficulty. Source: BitInfoCharts

Ethereum (ETH) hash rate & difficulty. Source: BitInfoCharts

Litecoin (LTC) hash rate & difficulty. Source: BitInfoCharts

Dash (DASH) hash rate & difficulty. Source: BitInfoCharts

Zcash (ZEC) hash rate & difficulty. Source: BitInfoCharts

DogeCoin (DOGE) hash rate & difficulty. Source: BitInfoCharts

Monero (XMR) hash rate & difficulty. Source: BitInfoCharts

ETH Shows Signs of Scaling Trouble

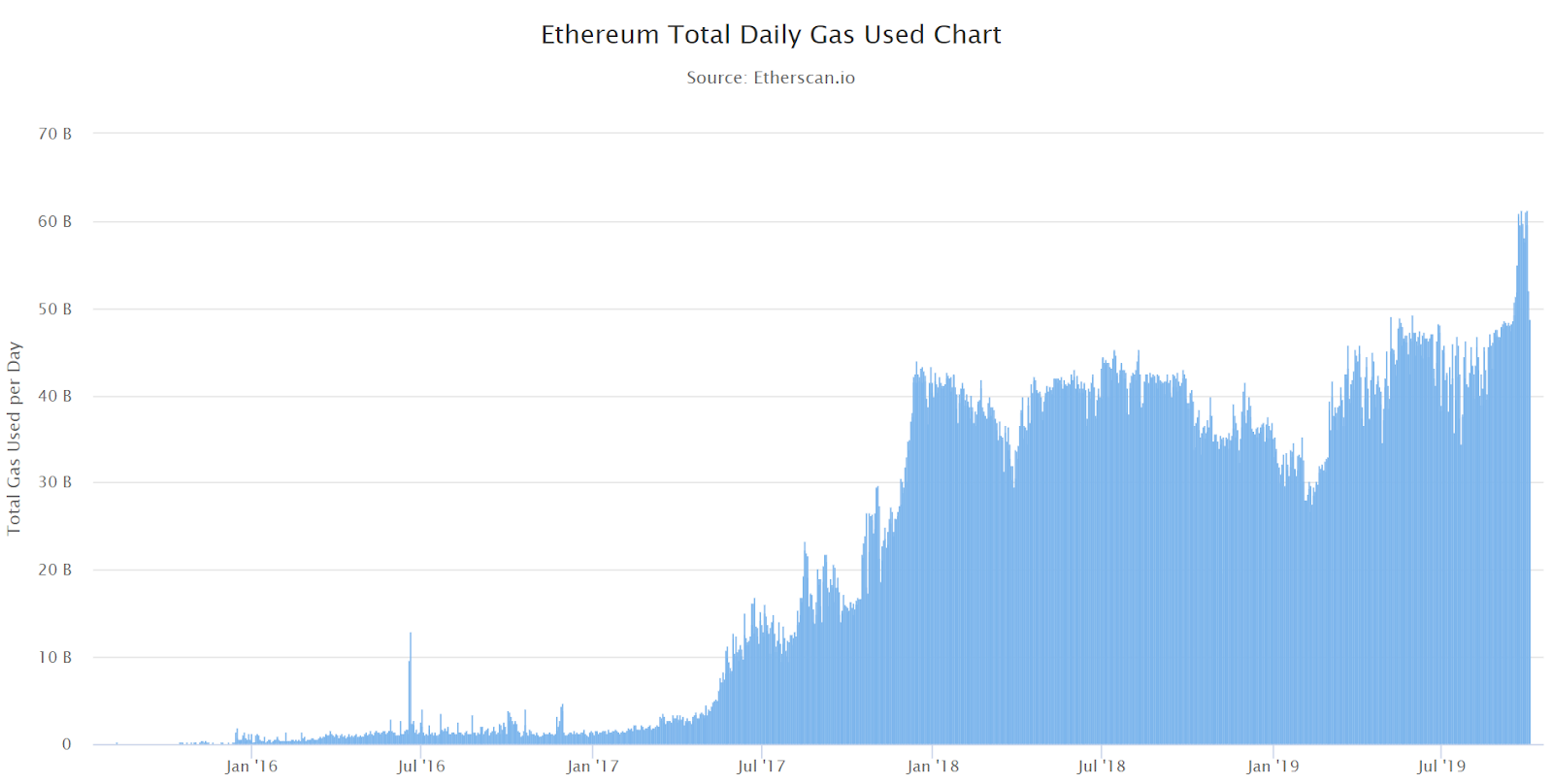

Despite the drop in total transactions per day, ETH saw fees rise near the end of Q3 due to a significant increase in smart contract activity.

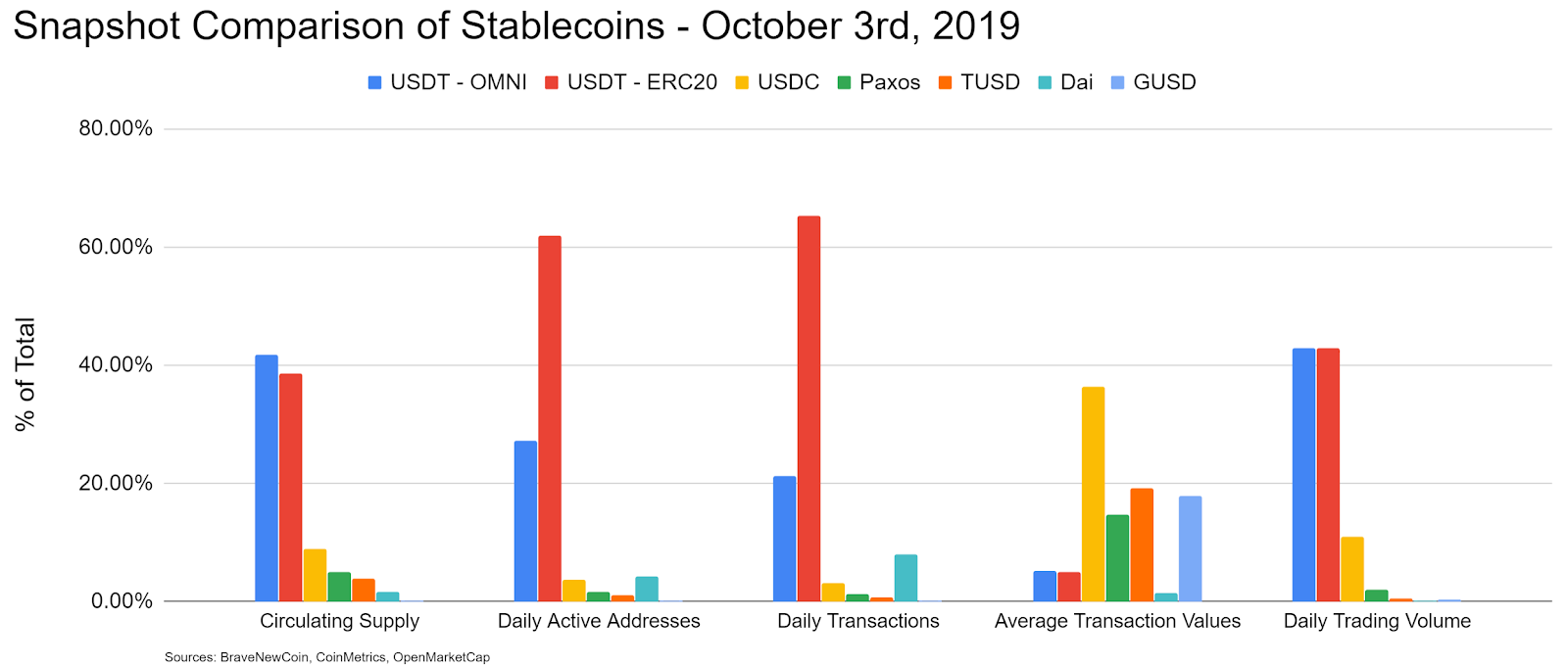

USDT was added to the ETH chain in January 2018 and adoption was slow initially, but has since increased rapidly as most exchanges have implemented this transfer option. USDT-ERC20 quickly become the dominant stablecoin medium of exchange, which means continued and increasing strain on ETH blockchain. USDT-OMNI circulating supply and transfer will likely continue to shrink because USDT transfers on ETH are both cheaper and quicker than OMNI.

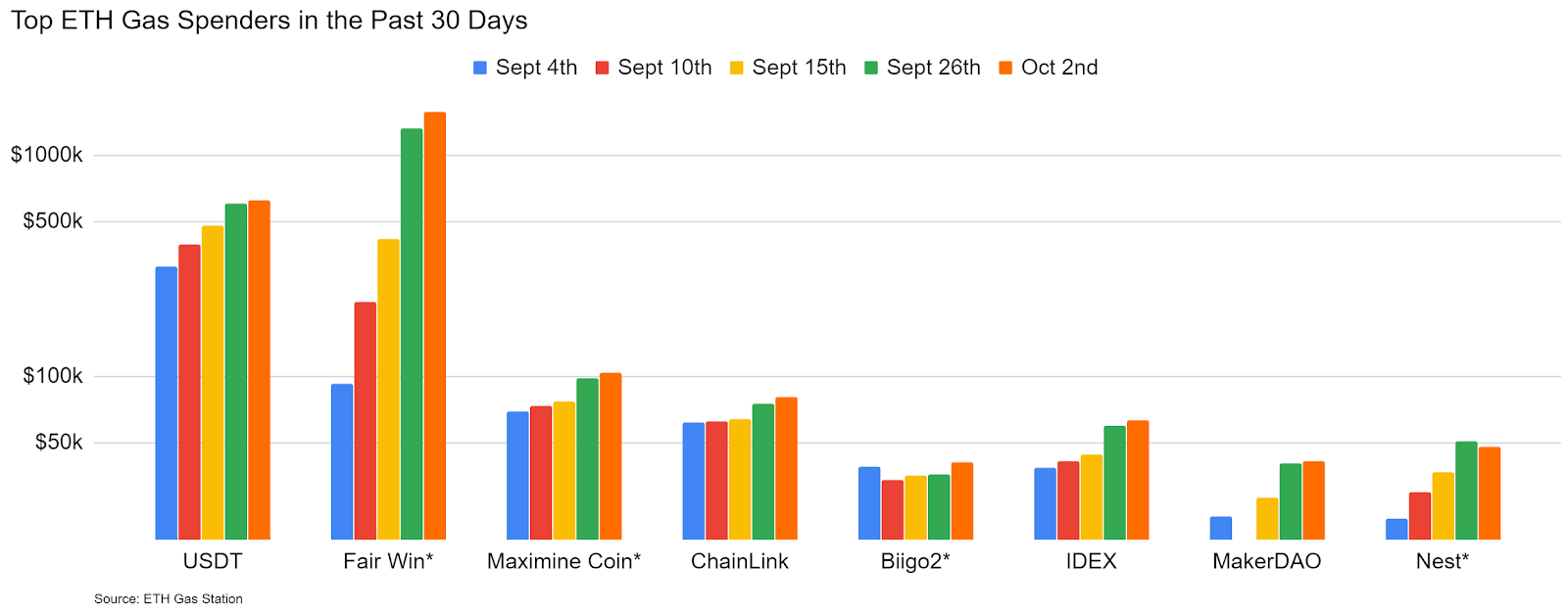

The Chinese Fair Win betting smart contract also saw a significant increase in transfer activity, so much so that it began to eclipse USDT in total gas costs over a 30-day period. Fair Win was valued at US$10 million with in 10 days of launching, before it quickly went to US$0, leading some to believe this was a Ponzi scheme, or exit scam.

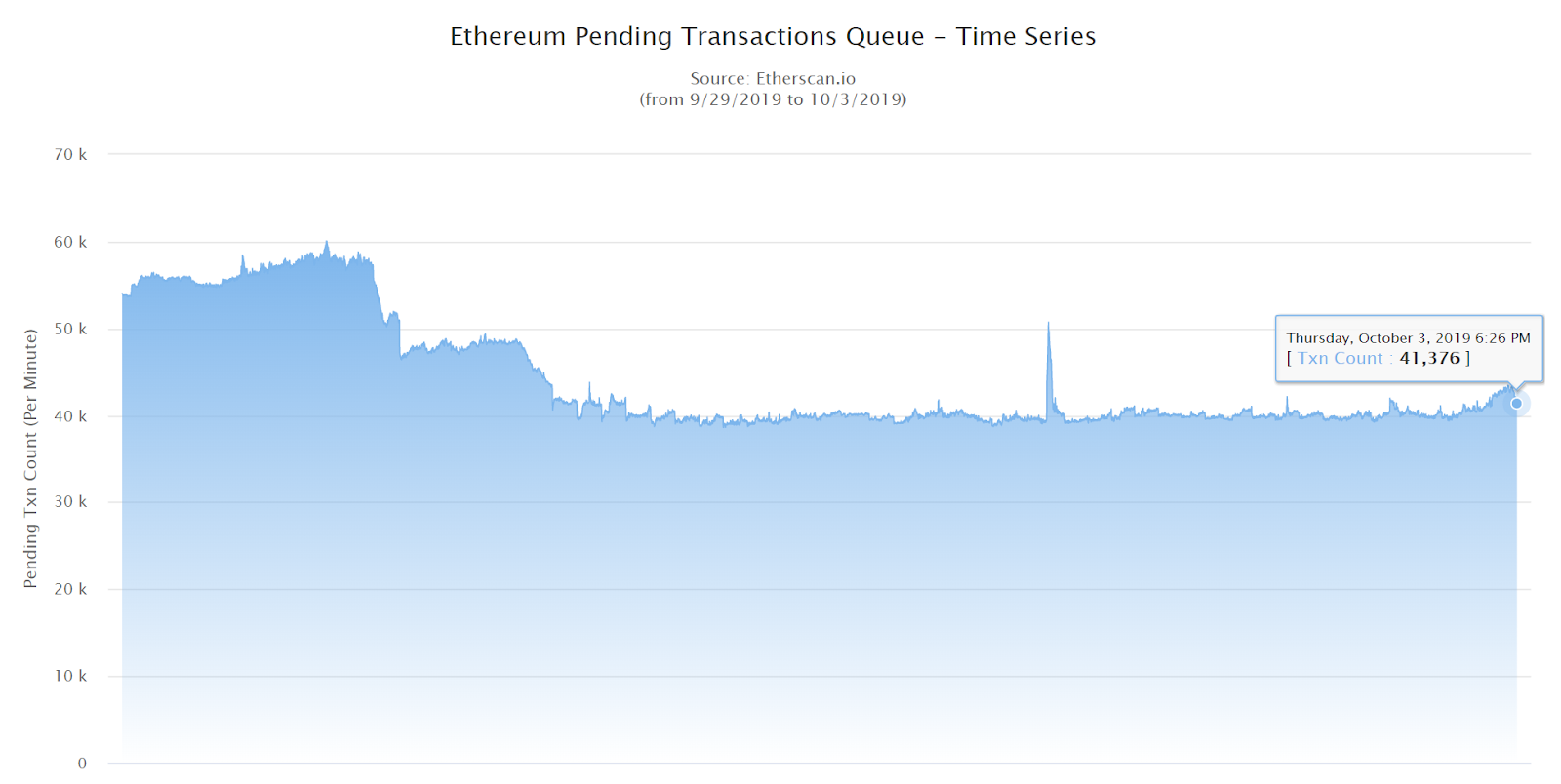

In September, ETH miners voted and agreed to raise the gas limits by 25%, enabling more transfers in a single block. The increased gas limits, and the end of the Fair Win smart contract, alleviated the high number of pending transactions on the chain, which exceeded 100,000. Gas usage spiked immediately after the limit raise, but has since declined to previous levels. Overall, this illustrates on-going scaling problems with smart contracts on the ETH chain. The scaling issue will ideally be improved by ETH 2.0 changes Casper and Sharding, set for a series of releases into 2022.

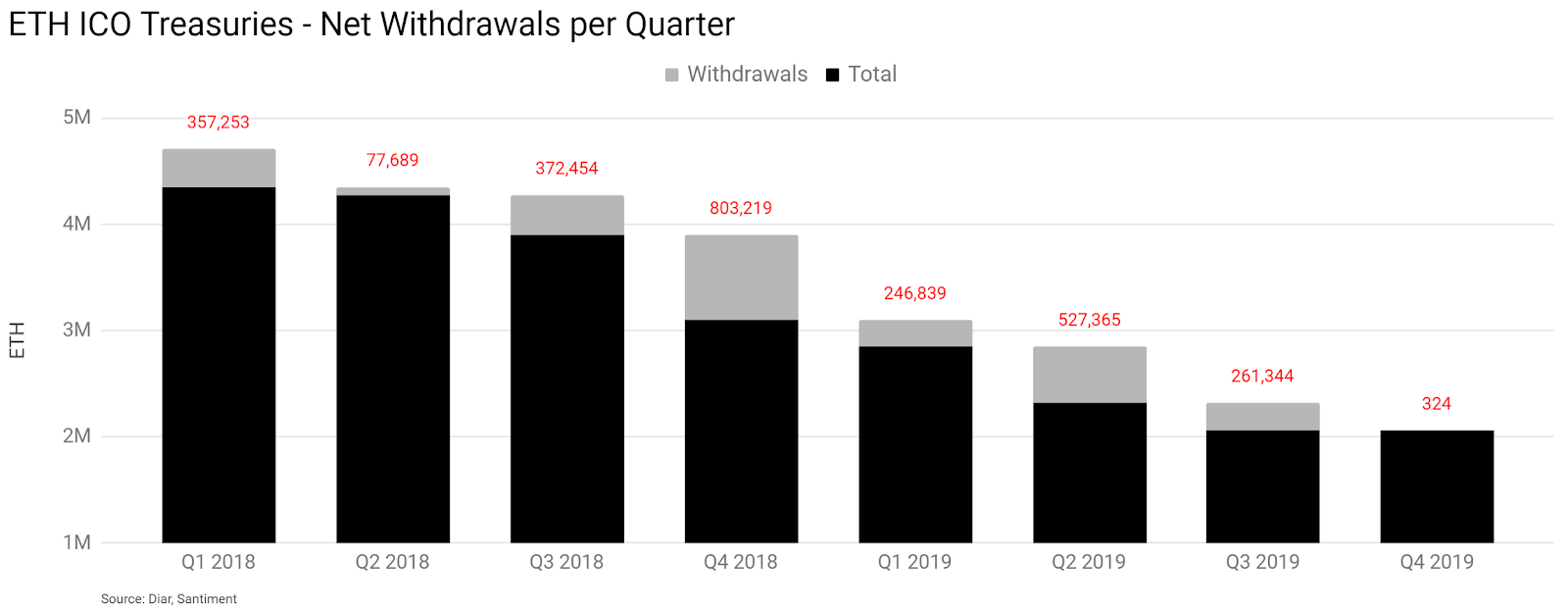

Initial Coin Offerings and Treasuries Continue to Decline

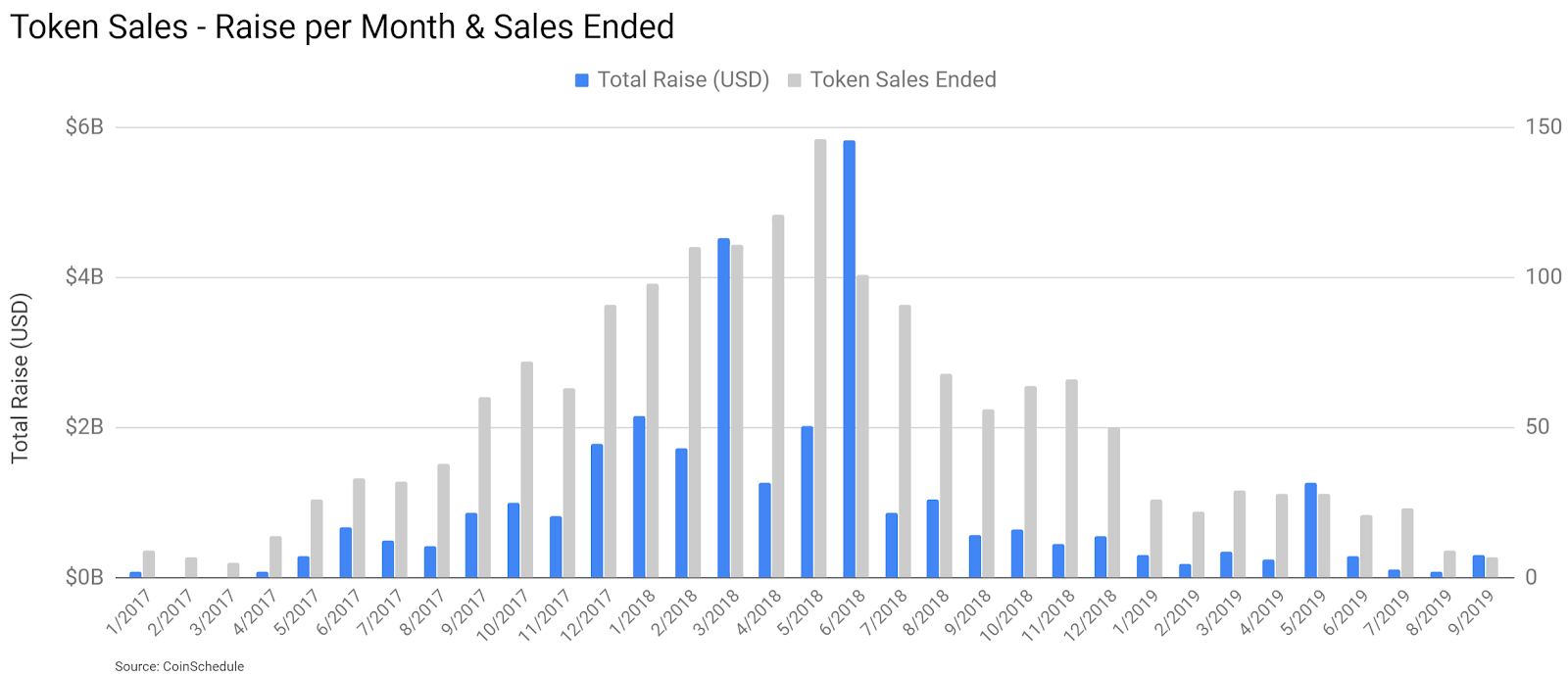

Initial Coin Offerings (ICOs) have largely been replaced with Initial Exchange Offerings (IEOs) as a means for projects to raise substantial capital. ICO treasuries continue to decrease as well, with just over two million ETH held by projects with transparent wallet addresses.

These IEOs are typically not on the ETH chain, but have served as a way for exchanges to generate additional fees for a listing and guaranteed trading pairs for the projects. The largest IEO thus far has been Bitfinex’s LEO token, which raised a reported US$1 billion in May, with LEO trading on the exchange shortly thereafter.

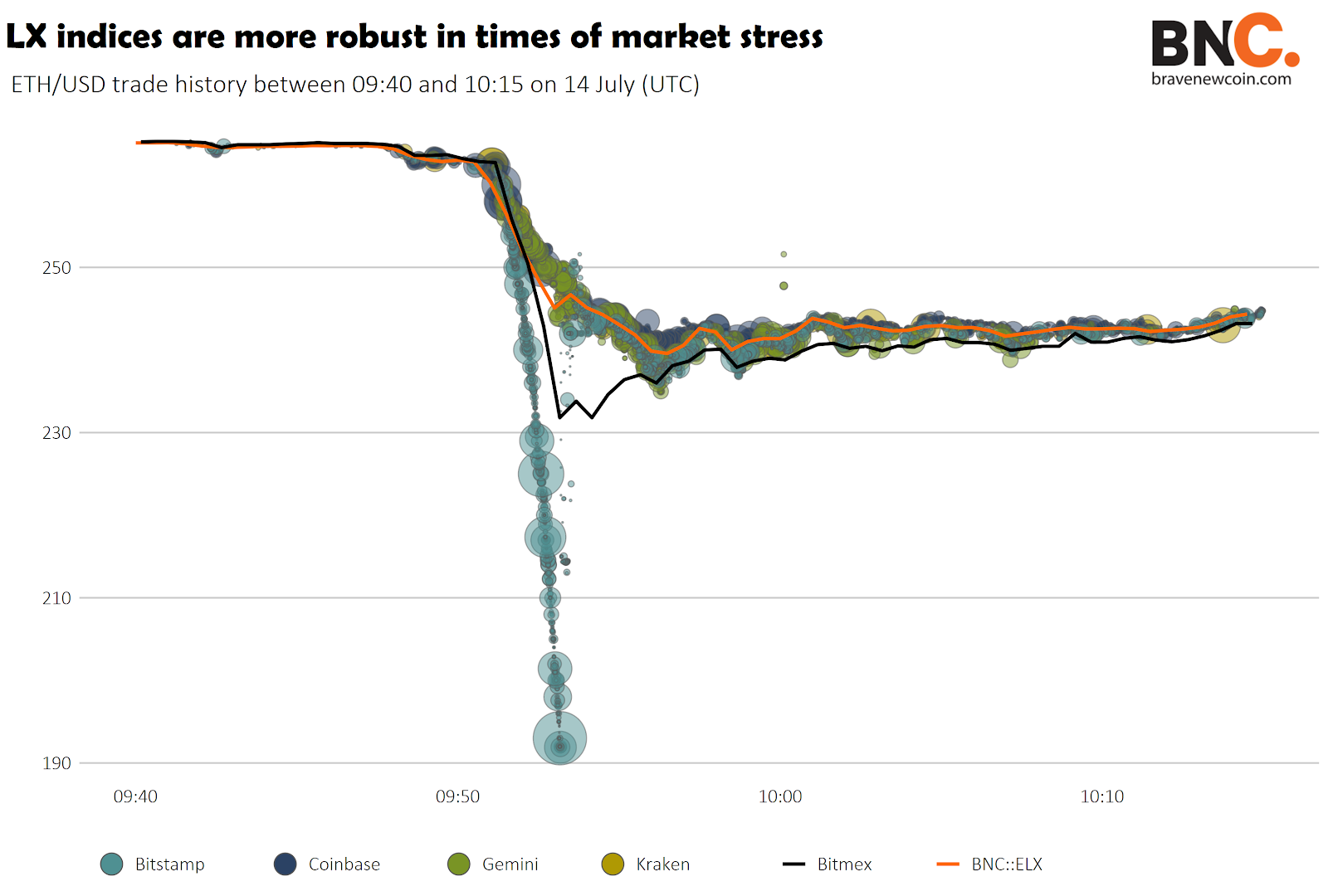

Another Bitstamp Flash Crash and Coinbase Technical Issues

Similar to the May 2019 BTC flash crash, Bitstamp experienced a quick and extreme market deviation on July 14th due to a series of large sell orders totalling around 15,500 ETH. The exchange was likely targeted for this market activity because Bitstamp is used as a constituent exchange in a number of indices on derivatives exchanges.

The crash liquidated US$17 million in notional value on Bitmex and also affected MakerDAO collateralized debt positions, 120 of which were liquidated on the move. Repeated incidents like this highlight the need to disincentivize the exploitation of weaknesses in exchange infrastructure with institutional grade indices, like the BNC BLX, to protect against market manipulation.

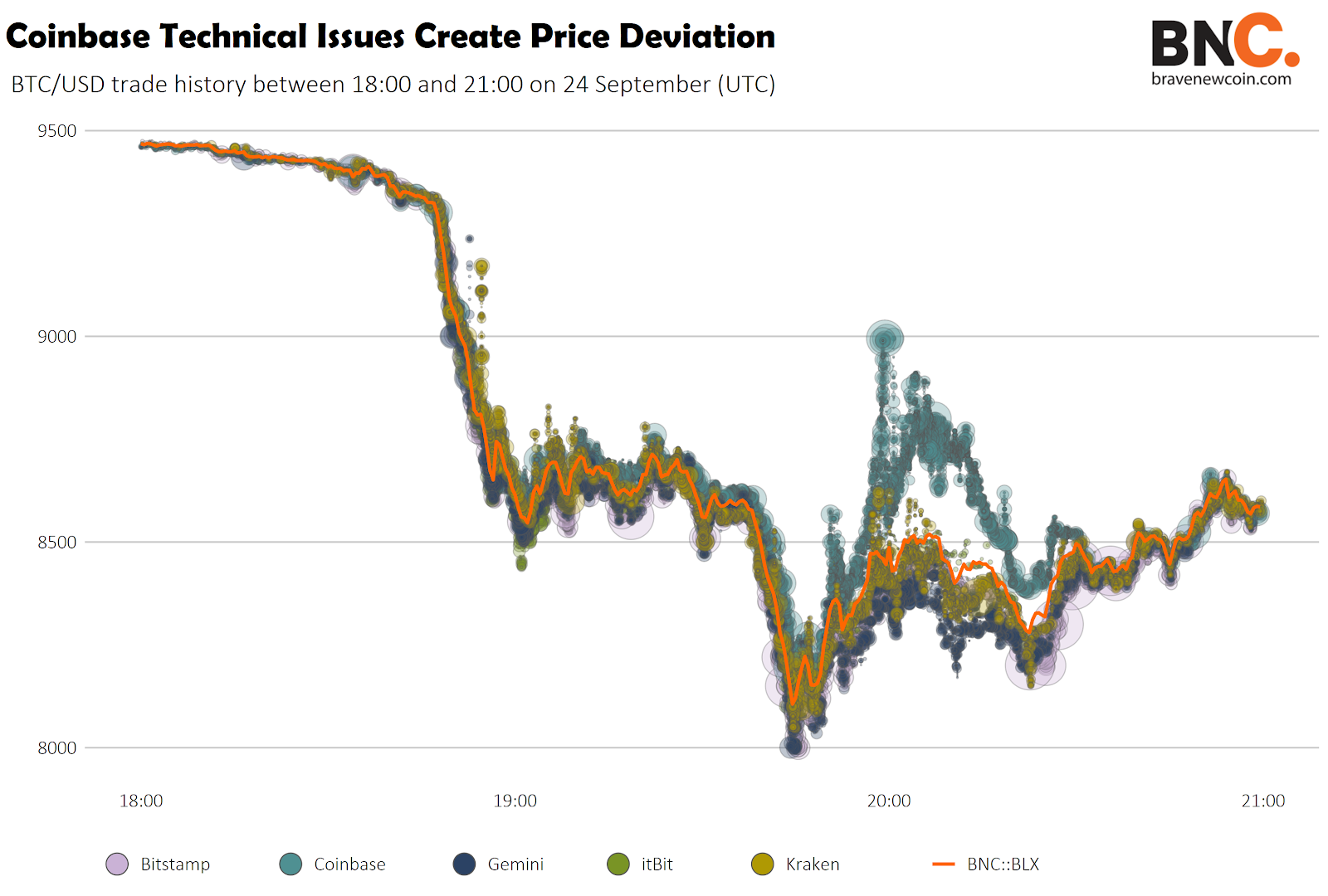

On September 24th, a BTC selling event caused a disconnect in price on the Coinbase exchange. Users were reporting a non-functioning orderbook at the time, with a large spread in prices. Coinbase Pro and Coinbase Prime also had a disconnected price for a short time period. Random and unpredictable events like this again illustrates the need for robust market indices for all products that rely heavily on accurate price information.

More Exchanges and Products Enter a Crowded Field

The much-hyped Bakkt, which raised US$182.5 million from 12 partners and investors in 2018, launched a physically delivered BTC futures product in late September. Thus far, trading volumes have been limited to less than 100 BTC per day. Bakkt is a subsidiary of the Intercontinental Exchange, which also runs the New York Stock Exchange. Starbucks also received a significant equity stake in the Bakkt BTC futures platform.

Bitfinex and Binance also launched derivatives markets this quarter. Binance also launched Binance.US which is geofenced for US citizens and currently lists 11 crypto assets. In September, VanEck-SolidX announced a limited version of a BTC ETF, available to qualified institutional buyers. The 144a product currently has US$521,000 under management. All other current U.S. BTC ETFs have been delayed or withdrawn completely.

Bitmex, which is currently under investigation by the U.S Commodity Futures Trading Commission, has also announced plans to launch a BTC zero coupon bond where users can earn a yield on their holdings by loaning BTC to other companies in the space. A Bitmex announcement in August also added further restrictions regarding access to the platform from users located in Hong Kong, Seychelles, and Bermuda due to regulatory concerns.

OhNoCrypto

via https://www.ohnocrypto.com

Josh Olszewicz, Khareem Sudlow